Orderly Transition: The complex case of residential batteries

By Joshua Stabler – Energy Edge Managing Director

Linked Articles: The Rise and Rise of Rooftop Solar

The trajectory of the development of battery solutions within Australia is shaping up to be one of the defining questions for the Australian energy market during the 2020’s and there are many evolving conditions that drive this statement. While the growth of this sector feels inevitable, there are still challenges ahead. Orderly transition is not assured and the cost of disorderly transition should not be underestimated.

The Complexity

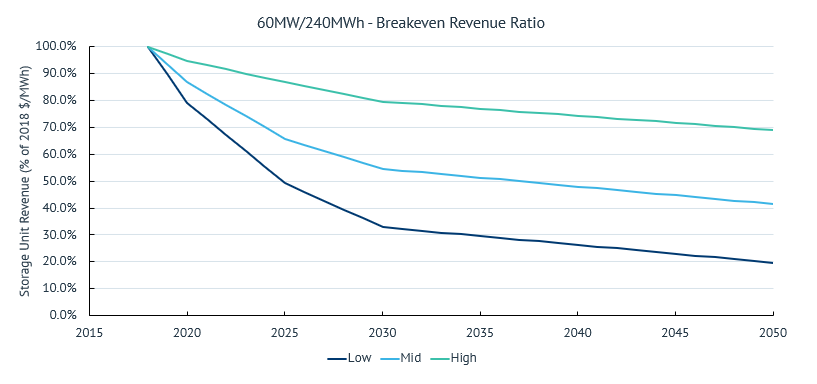

Firstly, the capital costs of batteries are continuing to decline rapidly due to steep learning curve improvements, equivalent to technologies like solar. While falling costs should be a keen benefit for the technology class, it does create a deflationary conundrum: Do you buy now? Or wait until later when it is cheaper?

Figure 1 – Breakeven Revenue Ratio for Large Scale Storage (Source: NREL, Lazard, Energy Edge)

Secondly, the avenues to market for batteries are broadening:

- Large Scale Batteries are characterised by their access to economies of scale, although revenues are based on the arbitrage in the wholesale markets and Frequency Control Ancillary Services (FCAS) markets.

- The early adopters will capture the highest revenues due to the least competition in this space, but these same assets will also be burdened with the highest ongoing capital costs (due to the falling cost curves).

- The next wave of competition joins the market favoured with a lower cost structure and reciprocally lower revenue threshold.

- The large-scale batteries compete with Pump Storage Hydro (or ‘shallow storage’ as per AEMO ISP definition) (further on this below).

- Residential Batteries are based behind the meter and their primary economic benefit is derived from the arbitrage between residential peak tariff and the solar feed-in tariff.

- This market is being driven by the growing systemic arbitrage between the higher evening peak tariff and the decline in the fair value of the solar feed-in tariffs (see The Rise and Rise of Solar Rooftop).

- One of the finer details here is that the wholesale energy price only makes up 30-40% of the residential tariff, which provides a systemic competitive advantage against large scale batteries (which must extract value from the wholesale market).

- The current range of technology (Tesla Powerwall) has a capacity of 13.5kWh.

- Electric Vehicles (EV) sharply increase the efficiency of transportation through the introduction of electric engines.

- In terms of efficiency, a Tesla 3 Long Range has a range of 637km based on 82kWh (290MJ) and a Toyota Camry (4-cylinder petrol) has a rated fuel efficiency of 8.3L (284MJ) per 100km. Therefore, a Tesla can provide 6.24x the travelled distance for the same energy content.

- Assuming the average annual residential car utilisation of 12,607km and a petrol price of $1.30/L, that is a potential saving of $1,142 p.a. based on fuel efficiency alone.

- However, a Toyota Camry also costs $29k to $39k compared with the $83k for a Tesla 3 Long Range so the benefits from fuel consumption do not yet solve the economics challenge alone.

- Finally, the Tesla 3 Long Range (82kWh) has 6x the energy storage capacity compared with the Tesla Powerwall (13.5kWh) at around 6x the price ($82k vs $13-15k), so the cost per kWh is the same.

AEMO Path Forward

AEMO’s Integrated System Plan (ISP) gives a vision of five potential paths forward for the Australian electricity market including:

- Central: the pace of transition is determined by market forces under current federal and state government policies.

- Slow Change: a slow-down of the energy transition, characterised by slower changes in technology costs, and low political, commercial, and consumer motivation to make the upfront investments required for significant emissions reduction.

- High Distributed Energy Resources (DER): more rapid, consumer-led transition, as consumers take control of their energy costs with easy-to-use, interactive technologies, falling costs for DER and EVs.

- Fast Change: a more rapid technology-led transition, its costs reduced by advancement in grid-scale technology and targeted policy support. There is coordinated national and international action to reduce emissions leads to innovation, automation, the accelerated exit of existing generators, and greater electric transport.

- Step Change: both consumer-led and technology-led transitions occur in the midst of aggressive global decarbonisation and strong infrastructure commitments.

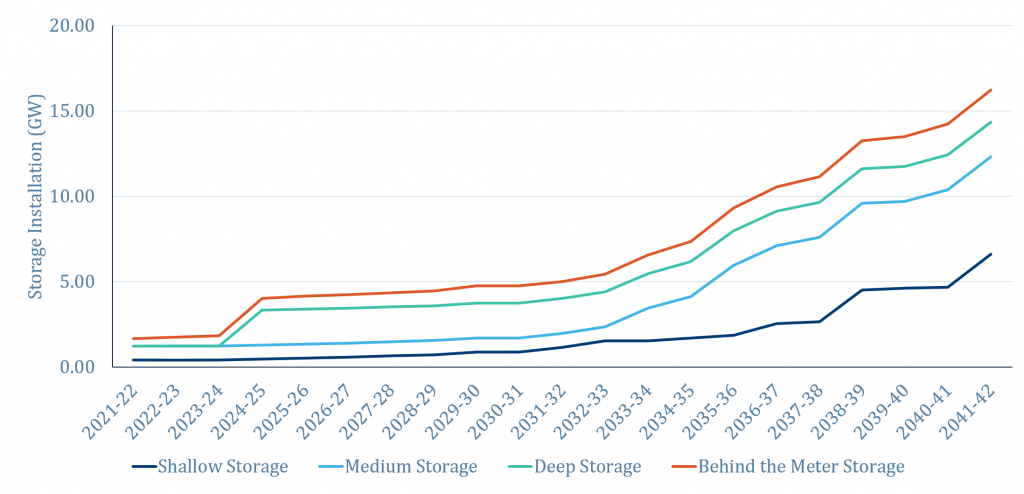

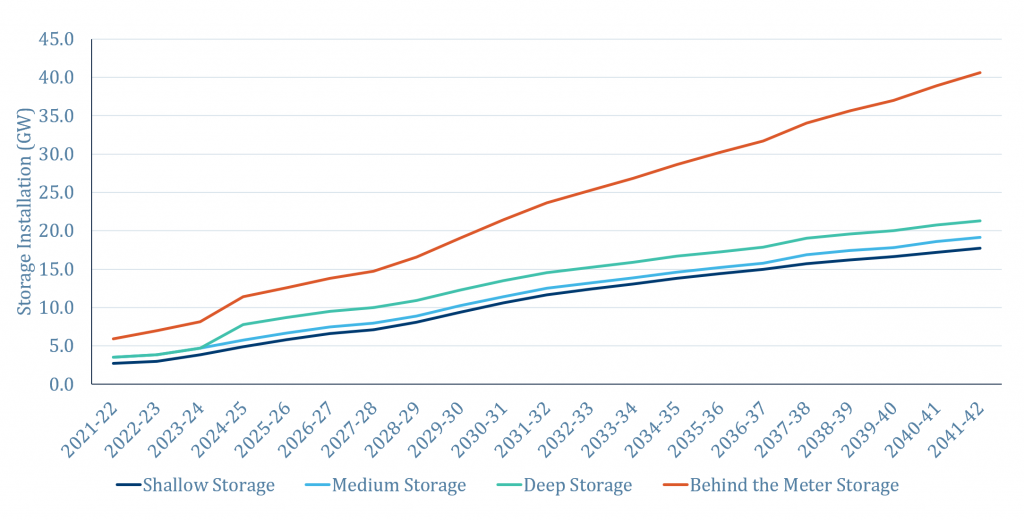

The following graphics shows two of those five paths with the Central case (Figure 2) and the High DER case (figure 3) where it can be noted that anticipated storage capacity for the Central case at 2040-41 (14GW) is the equivalent goal as 2027-28 in the High DER case.

Figure 2 – AEMO Integrated System Plan 2020 – Storage Investment – Central Case

Figure 3 – AEMO Integrated System Plan 2020 – Storage Investment – High DER Case

The different paths for batteries are very dependent on the continued growth of correlated solar and wind generators (as noted in our previous The Rise and Rise of Rooftop Solar) and the requirement to transiently shift capacity between the peaks and troughs of both diurnal and seasonal demand shapes.

However, the exact shape and technology of the storage solution is not etched in stone. The demand on the continued progression down the technology learning cost curves remains critical and the incentives for competitive alternative breakthroughs have never been higher.

After all of this article and the clear expectations on batteries, where is the complexity? Well, batteries only offer a path to an orderly transition if it can be achieved commercially. Without that final stipulation, it is just a dream.